- 04 Dec 2020 17:44

#15141062

So since Biden won, there have been quite a lot of buzz around the news and other media platforms regarding student loan forgiveness, in part because he has said he supports *some* degree of forgiveness. I think this is shaping to become another "third rail" in politics, alongside with SS, Healthcare, etc.

Disclaimer:

I am personally affected by this as I do have significant loans, although I am not "burdened" in the sense that I have the means to pay them within ~5y with moderate "intensity" or shorter (~3y?) if I focus everything on them. I don't want them "forgiven", I borrowed that money knowing I would have to give it back, and I got a great education that has value in exchange, I feel fortunate of having had this opportunity. That is not to say that if the government comes to me and tells me they are forgiven "x" amount of my balance, that I will not take it or I would reject that offer, I certainly won't and I would certainly be grateful for that.

and I would certainly be grateful for that.

However, I believe there is a middle ground between flat out "forgiving" money and doing nothing. I think a "small" modest forgiveness such as that proposed by Biden is going to be helpful to a lot of people that either dropped out of education (yet still have loans, but perhaps not as high as they didn't do full duration) or those that went to have a career within areas that don't really pay too much (teachers?).

But here is what I think might be just as helpful for those "higher-income earners" without making it a "handout", something that would be far more pallatable for more conservative-minded people. How about TAX credits for your loan replacement? For instance, every $$ you pay back towards your loans, it is a dollar that you don't have to pay a cent on taxes (or perhaps that it is taxed at a much lower rate?). This kind of thing is doable, we have the HSA (health saving accounts) which are accounts where you can put "pre-tax" money and use it towards health expenses. For someone in high income, who perhaps is in the 30-40% tax bracket, using this account for glasses or the dentist, for instance, could amount to 40% savings!

Within the paradigm in which 100% of the money I pay towards my loans is "tax free" or "pre-tax", the time it would take me to pay my loans would essentially half, as close to 40% of the income I currently have, is going for taxes.

Furthermore, this could also be tailored towards "facilitating" payments vs defaults. How so? Well, you could put a time limit for this "benefit" to apply. For instance, you could say... The moment that this law takes into effect, it will cover all borrowers regardless of graduation date, for (lets say) 5 years. So we now all have 5 years to pay as much (or hopefully all) our student debt. If we don't, then, whatever reminder balance would have to be paid without the benefit of this tax break/credit/deduction. However, anybody that graduates into the future would have the "timer" start ticking, right after graduation (the lending programs already track this, as many give a 6M grace period after graduation and/or go into deferment if you go back to school).

This system, would not be a "handout", you are literally paying everything back with your own money and your own sweat. However, it would be a huge "discount" for most people, perhaps up to 40%.

This approach also allows for methods of facilitating parents towards paying for their kid's education as you could make it so that immediate family could help tax free for up to a limit amount.

Finally, you can also make it significantly easier for the "public" loan forgiveness. For instance... 5 years instead of 10. Currently this kind of program is not very attractive to a lot of people, in part because you have to commit a decade for something that it is notoriously difficult to get right, it is a lot of commitment. Within my field, I see people with high debt, that you would naturally think would be attracted to this, not interested on the program, in part because of how long it is. For instance, a hand surgeon with 500k in student debt is not attracted to an job position in a rural service that pays 400k /year for his skills, because he can easily go to group that would pay twice that, and despite the increase in tax burden, the difference in salary easily pays the 500k student debt in much shorter time than the 10y that would take to take advantage of the student loan forgiveness plan. However, if the duration is lowered, the math becomes far more favorable. Again... this is not a handout... people with high skills are desperately needed in rural areas. A hand, orthopedic, plastic surgeons in a rural area of Washington or Montana where you might have a logging accident could be the difference between losing an arm or having a terrible scar/disability/chronic pain vs much better recovery/outcome.

Then there is the issue with interests. This is another area that can significantly help borrowers, and this is something that can be done relatively quick and painless.

All of this does not mean that a "small" amount "forgiven". But perhaps a multi-prong attack is more beneficial, yet palatable to those in congress and their supporters.

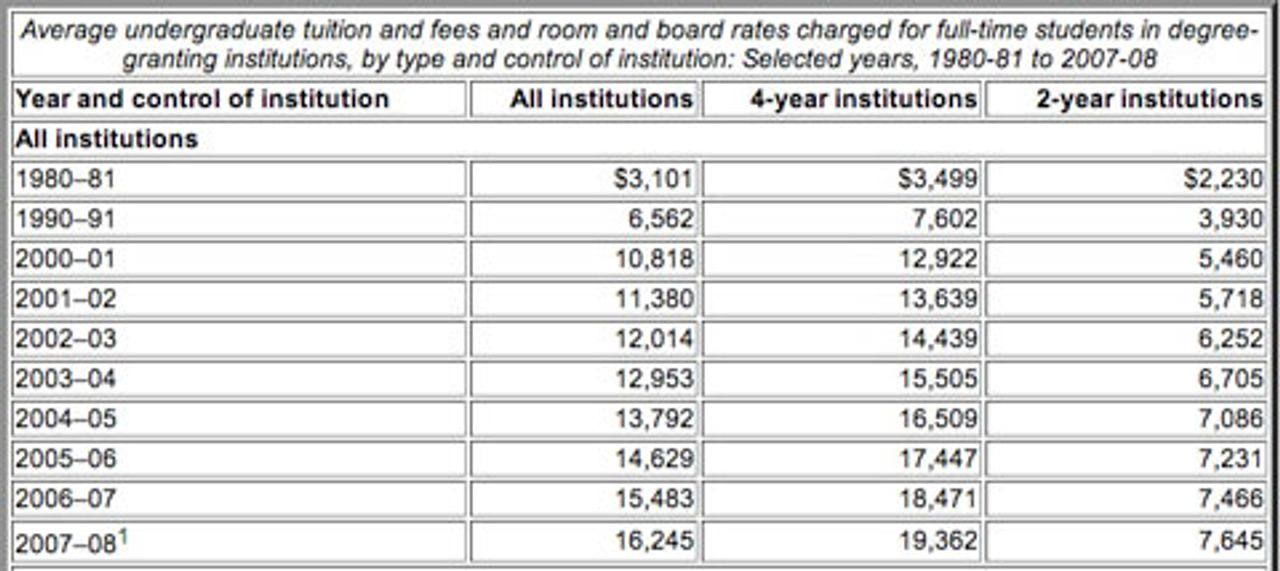

Finally, there is the issue of addressing the skyrocketing costs of higher education. I won't touch the topic just yet but this certainly needs addressing as well.

Disclaimer:

I am personally affected by this as I do have significant loans, although I am not "burdened" in the sense that I have the means to pay them within ~5y with moderate "intensity" or shorter (~3y?) if I focus everything on them. I don't want them "forgiven", I borrowed that money knowing I would have to give it back, and I got a great education that has value in exchange, I feel fortunate of having had this opportunity. That is not to say that if the government comes to me and tells me they are forgiven "x" amount of my balance, that I will not take it or I would reject that offer, I certainly won't

and I would certainly be grateful for that.However, I believe there is a middle ground between flat out "forgiving" money and doing nothing. I think a "small" modest forgiveness such as that proposed by Biden is going to be helpful to a lot of people that either dropped out of education (yet still have loans, but perhaps not as high as they didn't do full duration) or those that went to have a career within areas that don't really pay too much (teachers?).

But here is what I think might be just as helpful for those "higher-income earners" without making it a "handout", something that would be far more pallatable for more conservative-minded people. How about TAX credits for your loan replacement? For instance, every $$ you pay back towards your loans, it is a dollar that you don't have to pay a cent on taxes (or perhaps that it is taxed at a much lower rate?). This kind of thing is doable, we have the HSA (health saving accounts) which are accounts where you can put "pre-tax" money and use it towards health expenses. For someone in high income, who perhaps is in the 30-40% tax bracket, using this account for glasses or the dentist, for instance, could amount to 40% savings!

Within the paradigm in which 100% of the money I pay towards my loans is "tax free" or "pre-tax", the time it would take me to pay my loans would essentially half, as close to 40% of the income I currently have, is going for taxes.

Furthermore, this could also be tailored towards "facilitating" payments vs defaults. How so? Well, you could put a time limit for this "benefit" to apply. For instance, you could say... The moment that this law takes into effect, it will cover all borrowers regardless of graduation date, for (lets say) 5 years. So we now all have 5 years to pay as much (or hopefully all) our student debt. If we don't, then, whatever reminder balance would have to be paid without the benefit of this tax break/credit/deduction. However, anybody that graduates into the future would have the "timer" start ticking, right after graduation (the lending programs already track this, as many give a 6M grace period after graduation and/or go into deferment if you go back to school).

This system, would not be a "handout", you are literally paying everything back with your own money and your own sweat. However, it would be a huge "discount" for most people, perhaps up to 40%.

This approach also allows for methods of facilitating parents towards paying for their kid's education as you could make it so that immediate family could help tax free for up to a limit amount.

Finally, you can also make it significantly easier for the "public" loan forgiveness. For instance... 5 years instead of 10. Currently this kind of program is not very attractive to a lot of people, in part because you have to commit a decade for something that it is notoriously difficult to get right, it is a lot of commitment. Within my field, I see people with high debt, that you would naturally think would be attracted to this, not interested on the program, in part because of how long it is. For instance, a hand surgeon with 500k in student debt is not attracted to an job position in a rural service that pays 400k /year for his skills, because he can easily go to group that would pay twice that, and despite the increase in tax burden, the difference in salary easily pays the 500k student debt in much shorter time than the 10y that would take to take advantage of the student loan forgiveness plan. However, if the duration is lowered, the math becomes far more favorable. Again... this is not a handout... people with high skills are desperately needed in rural areas. A hand, orthopedic, plastic surgeons in a rural area of Washington or Montana where you might have a logging accident could be the difference between losing an arm or having a terrible scar/disability/chronic pain vs much better recovery/outcome.

Then there is the issue with interests. This is another area that can significantly help borrowers, and this is something that can be done relatively quick and painless.

All of this does not mean that a "small" amount "forgiven". But perhaps a multi-prong attack is more beneficial, yet palatable to those in congress and their supporters.

Finally, there is the issue of addressing the skyrocketing costs of higher education. I won't touch the topic just yet but this certainly needs addressing as well.

")

- By wat0n

- By wat0n - By Godstud

- By Godstud